Updated: 2025-02-04

In the 2024 federal budget, the Department of Finance announced an increase to the capital gains inclusion rate from one half (1/2) to two thirds (2/3) for capital gains realized after June 24, 2024. This increase applies to all types of corporations. However, an individual, a graduated rate estate (GRE) or a qualified disability trust (QDT) are eligible to have a reduced inclusion rate applied to their capital gains under the $250,000 threshold from the basic inclusion rate of two thirds to one half.

As of the date of writing this documentation, the increased inclusion rate has been deferred to January 1, 2026. As such, the 2/3 rate does not apply. Please read Deferral in Implementation of Change to Capital Gains Inclusion Rate for the most up-to-date information on the proposed changes to the capital gains inclusion rate. See also the T2 Schedule 6 and the Capital Gains Inclusion Rate.

If you choose to apply the new 2/3 capital gains inclusion rate, TaxCycle automatically applies the new inclusion rate in the capital dividend account (CDA) calculation in the CDA worksheets and T2054, as well as Schedule 89, by taking into account the new inclusion rate on amount M4 in Part 9 of the Schedule 6.

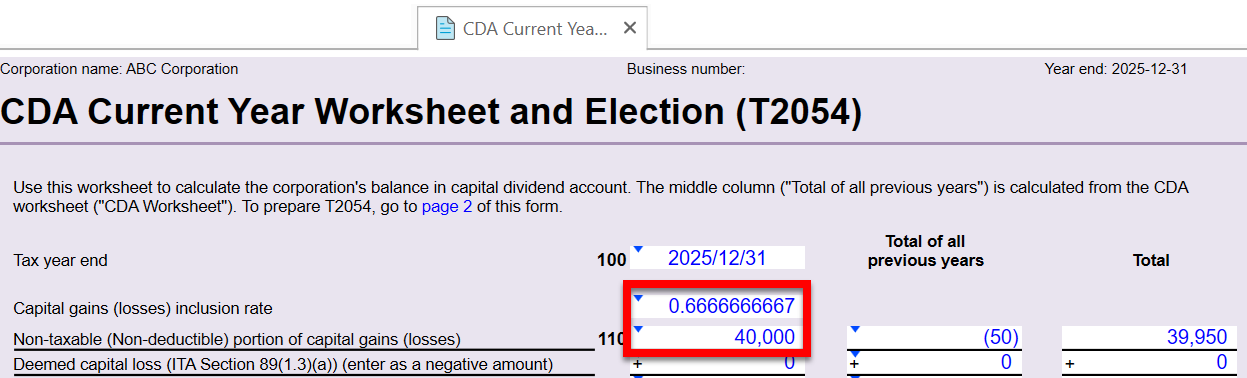

For example, if a private corporation’s only disposition is a post-June 24, 2024, transaction, which results in a capital gain of $120,000, the non-taxable portion of the capital gain ($40,000) is calculated as $120,000 x (1 - 2/3) = $40,000.

Where a corporation carries back a capital loss from a subsequent taxation year to a previous taxation year with a different capital gains inclusion rate, the CDA calculation must be adjusted at year-end to reconcile the difference in the inclusion rates (Deemed Capital Loss adjustment under ITA 89(1.3)(a)).

In the same token, where a corporation carries forward and utilizes an unused capital loss from a previous taxation year to a subsequent taxation year with a different capital gains inclusion rate, a similar year-end adjustment must be made to the CDA balance (Deemed Capital Gain adjustment under ITA 89(1.3)(b)).

To accommodate the adjustments under the two above deeming rules, the following new fields and section have been added to the CDA Current Year worksheet:

Read the examples below for more detailed information on how to calculate the CDA adjustments at year-end.

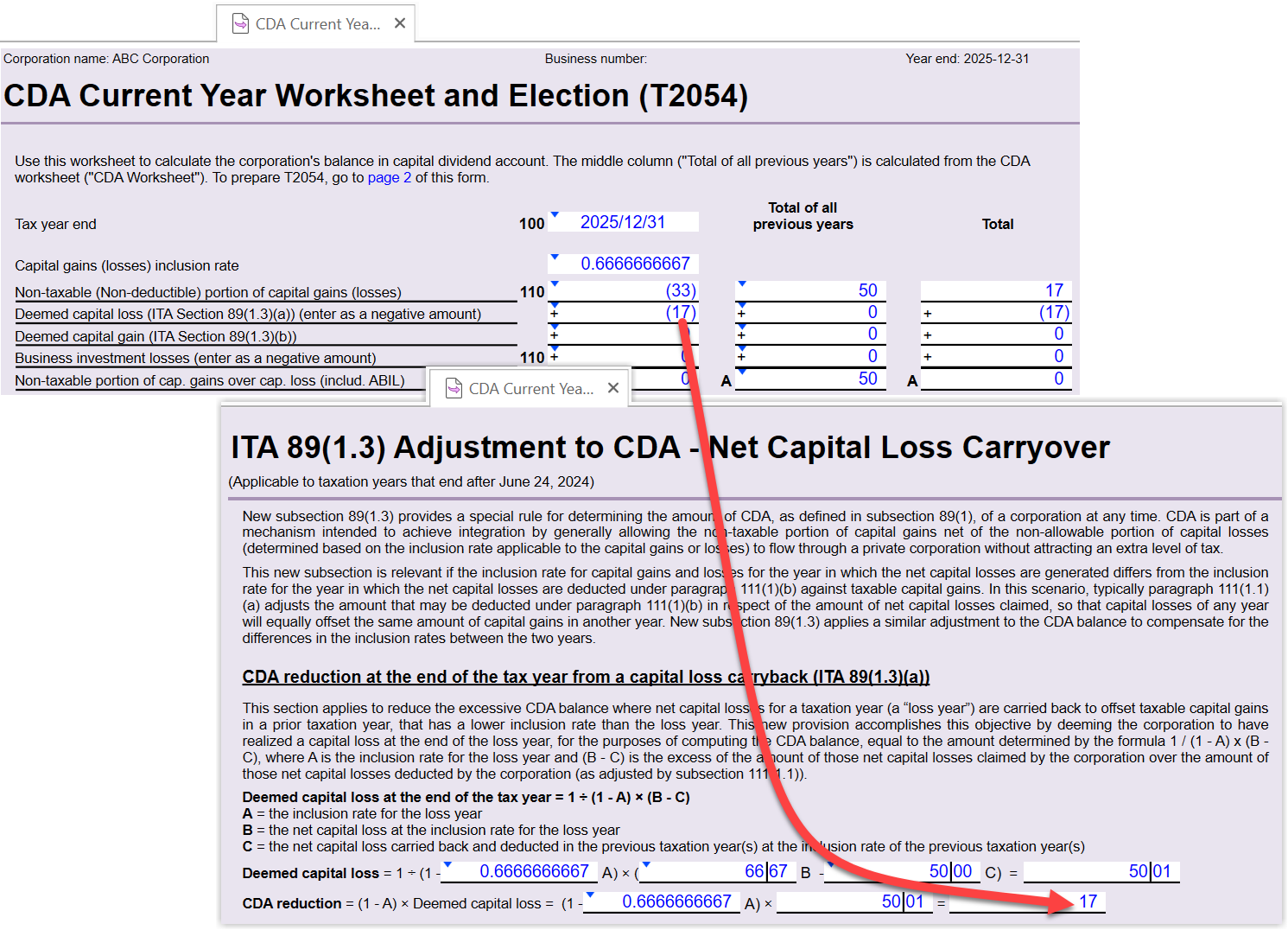

Deemed Capital Loss from a Capital Loss Carryback (ITA 89(1.3)(a))

Where the net capital losses (“NCL”) for a taxation year (a “loss year”) are carried back to offset taxable capital gains in a prior taxation year with a lower inclusion rate than the loss year (i.e., Capital loss in 2025 (2/3 rate) is carried back to offset a capital gain in 2023 (1/2 rate)), the proposed ITA 89(1.3)(a) deems the corporation to have realized a capital loss at the end of the loss year (i.e., 2025), for the purposes of computing the CDA balance.

Example: Deemed capital loss under ITA 89(1.3)(a)

Year 2025 = $100 of capital loss (carry back to 2023)

Year 2023 = $100 of capital gain

(A sample file “ABC Corporation_Deemed Capital Loss.2024T2” can be found in the installation folder C:\Program Files (x86)\Trilogy Software\TaxCycle\Samples)

A private corporation realized $100 of capital gains in 2023 (where the inclusion rate was 1/2, the taxable capital gains were $50) and $100 of capital losses in 2025 (where the inclusion rate was 2/3, the allowable capital losses were $66.67). The corporation’s 2025 NCLs are equal to the amount of its allowable capital losses of $66.67. In order to completely offset the capital losses with the capital gains, the corporation must claim all $66.67 of its 2025 NCLs under paragraph 111(1)(b) for its 2023 taxation year because subsection 111(1.1) reduces the deduction to $50 ($66.67 x (1/2)/(2/3)).

However, without any further adjustments, the corporation would end up with an excessive CDA balance of $16.67 (the non-taxable portion of the capital gains of $50 ($100 - $50) less the non-allowable portion of the capital losses of $33.33 ($100 – $66.67)).

Since the corporation’s NCLs for the loss year (2025) are carried back to offset capital gains in a prior year that has a lower inclusion rate (2023), for the purposes of computing the corporation’s CDA balance, new paragraph 89(1.3)(a) deems the corporation to have realized a capital loss of $50, determined by the formula 1 / (1 - A) x (B - C), or 1/(1 - 2/3) x ($66.67 – $50).

A = the inclusion rate for the loss year = 2/3

B = the NCL at the inclusion rate for the loss year = $66.67 ($100 x 2/3)

C = the NCL carried back and deducted at the previous tax year’s inclusion rate = $50 ($100 x 1/2)

Consequently, the CDA balance is reduced by $16.67, equal to the non-allowable portion of the deemed capital loss ($50 – (2/3 of $50)). This reduction eliminates the excessive CDA balance generated by the capital gains realized in 2023 that was offset against capital losses in 2025.

For the above example, TaxCycle calculates and displays the adjustment as follows (a sample file “ABC Corporation_Deemed Capital Loss.2024T2” can be found in the installation folder C:\Program Files (x86)\Trilogy Software\TaxCycle\Samples):

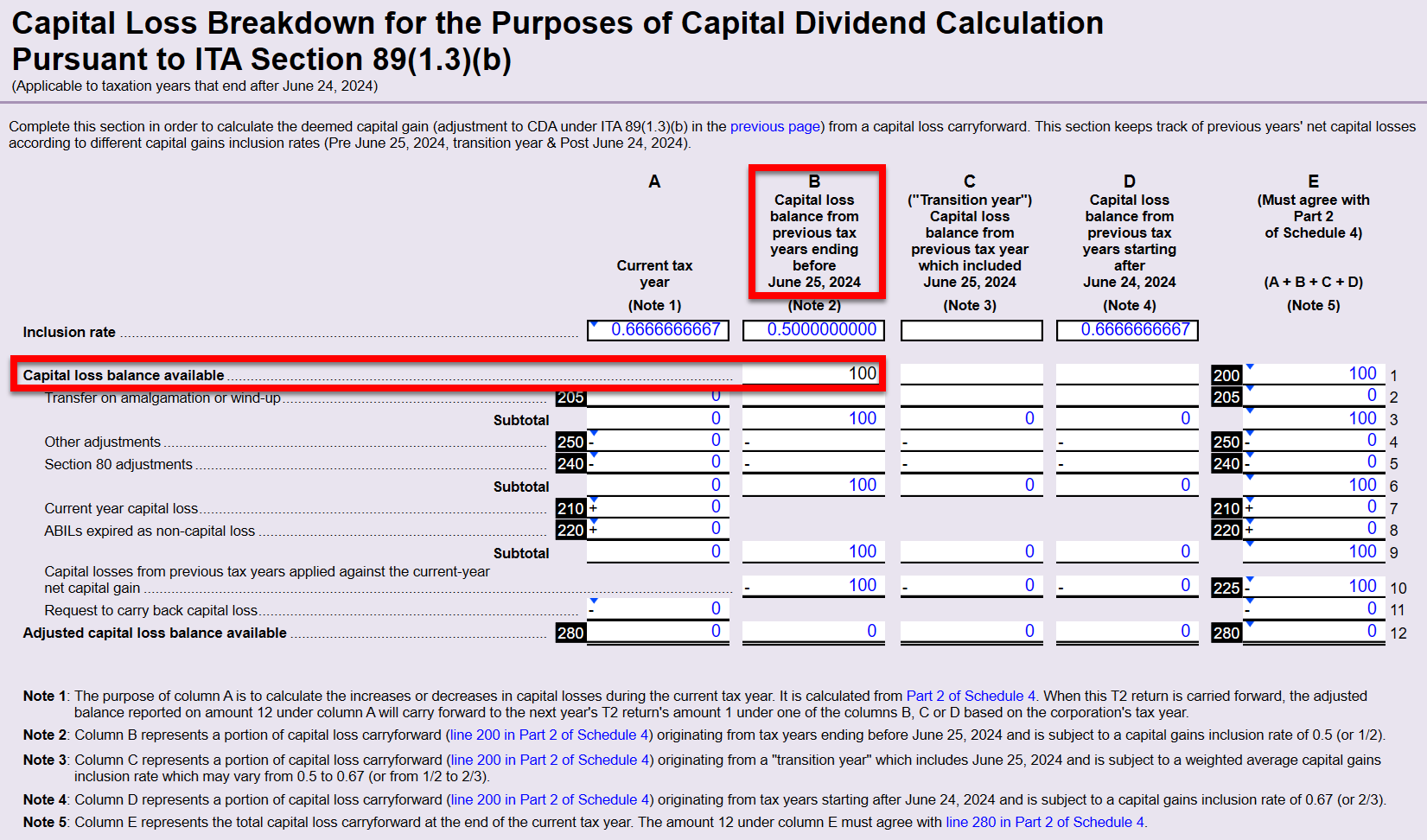

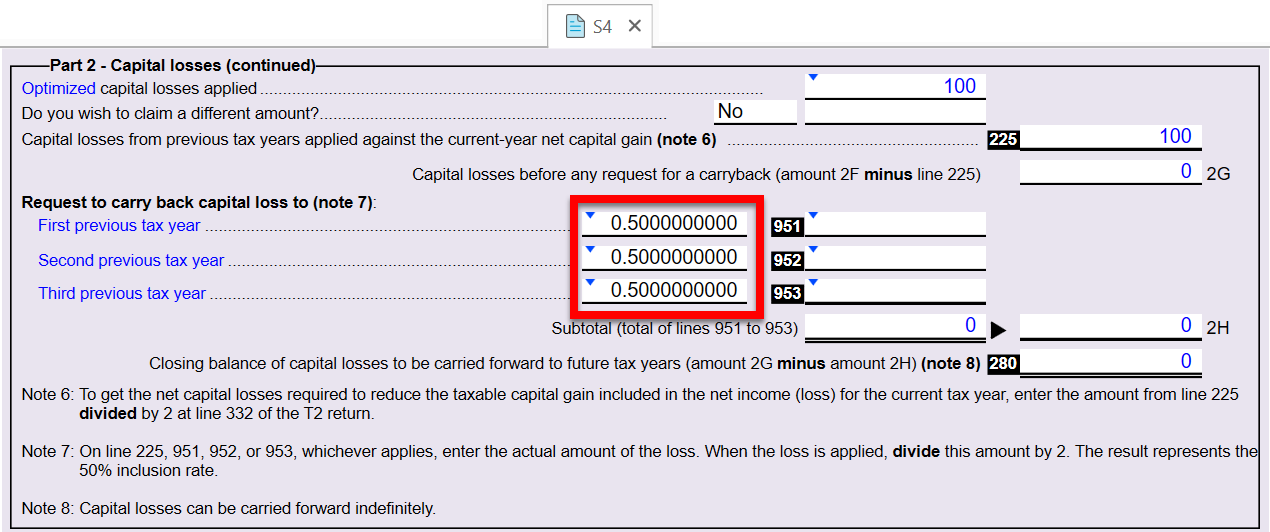

Schedule 4 (S4) now includes the following new fields in order to keep track of the previous years’ inclusion rates and to calculate the net capital loss carried back and deducted at the previous tax year’s inclusion rate (variable C).

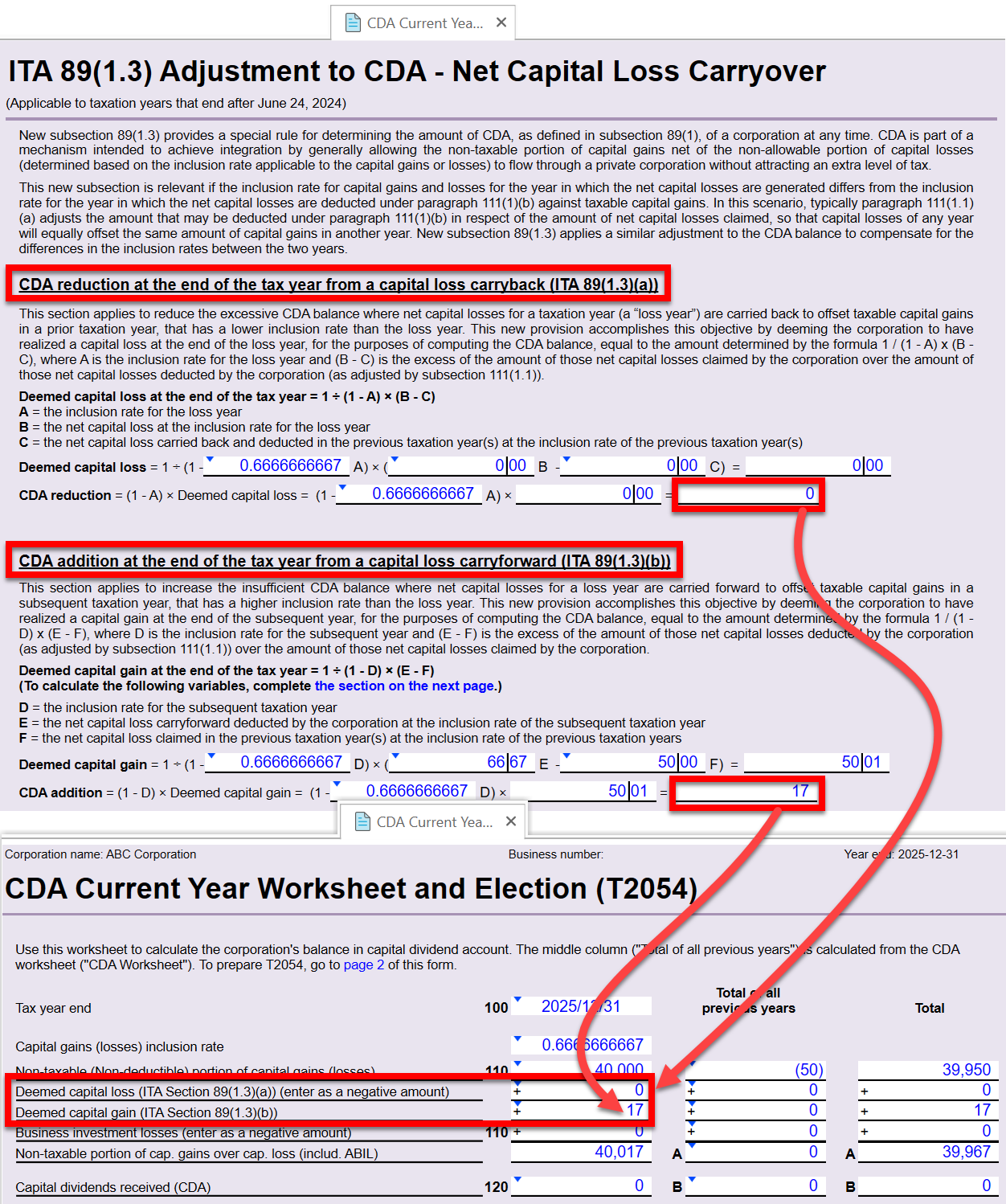

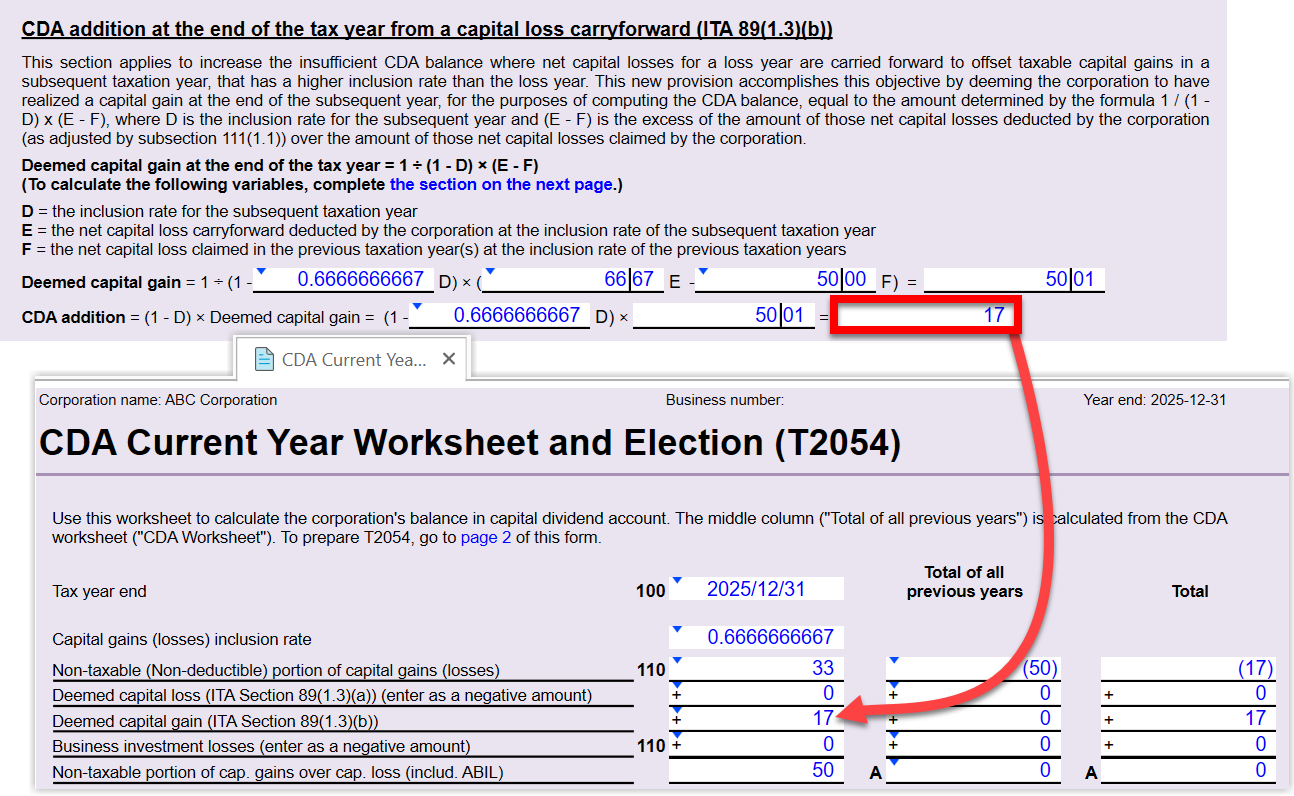

Deemed Capital Gain from Utilization of Capital Loss Carryforward (ITA 89(1.3)(b))

Where the net capital losses (“NCL”) for a taxation year (a “loss year”) are carried forward to offset taxable capital gains in a subsequent taxation year with a higher inclusion rate than the loss year (i.e., Capital loss in 2023 (1/2 rate) is carried forward to offset a capital gain in 2025 (2/3 rate)), the proposed ITA 89(1.3)(b) deems the corporation to have realized a capital gain at the end of the subsequent year, for the purposes of computing the CDA balance. The mechanics of the year-end adjustment is the exact opposite of the proposed legislation under ITA 89(1.3)(a) which was discussed in the previous section and example.

Example: Deemed capital gain under ITA 89(1.3)(b)

Year 2025 = $100 of capital gain (offset by capital loss from 2023)

Year 2023 = $100 of capital loss

(A sample file “ABC Corporation_Deemed Capital Gain.2024T2” can be found in the installation folder C:\Program Files (x86)\Trilogy Software\TaxCycle\Samples)

A private corporation realized $100 of capital losses in 2023 (i.e. “loss” year where the inclusion rate was 1/2, the allowable capital losses were $50) and $100 of capital gains in 2025 (where the inclusion rate was 2/3, the taxable capital gains were $66.67)). The corporation’s 2023 NCLs are equal to the amount of its allowable capital losses of $50. In order to completely offset the capital gains with the capital losses, the corporation must utilize all of the unused $50 of its 2023 NCLs for its 2025 taxation year to offset taxable capital gains of $66.67 in 2025.

However, without any further adjustments, the corporation would end up with a negative CDA balance of $16.67 (non-allowable portion of the capital loss of $50 ($100 - $50) less the non-taxable portion of the 2025 capital gains of $33.33 ($100 – $66.67)).

So, for the purposes of computing the corporation’s CDA balance, new paragraph (b) deems the corporation to have realized a capital gain of $50, determined by the formula 1 / (1 - D) x (E - F), or 1/(1 - 2/3) x ($66.67 – $50).

D = the inclusion rate for the subsequent taxation year (i.e., 2/3 in 2025)

E = the NCL deducted at the inclusion rate of the subsequent taxation year = $66.67 ($100 x 2/3)

F = the NCL at the previous “loss” year’s inclusion rate = $50 ($100 x 1/2)

Consequently, the CDA balance is increased by $16.67. This addition eliminates the deficiency of the CDA balance generated by the capital gains realized in 2025 that was offset by the unused capital loss carryforward from 2023.

For the above example, TaxCycle calculates and displays the adjustment as follows (a sample file ‘’ABC Corporation_Deemed Capital Gain.2024T2“ can be found in the installation folder):

In order to adjust CDA for the effect of unused capital loss carryforward from a period with a different inclusion rate, a new section has been added to the CDA Current Year worksheet to track capital losses by different inclusion rates.

When you open an existing return, TaxCycle automatically takes the unused capital loss carry forward from line 102 of the Schedule 4 (S4) and automatically populates it to column B of the CDA Current Year worksheet (assuming that unused capital loss carry forward has originated from the period before June 25, 2025, using the 1/2 inclusion rate).

If you are preparing a new T2 return for an existing file without a carryforward, you must enter the balance from line 102 of the S4 manually in column B of the new section of the CDA Current Year worksheet.