TaxCycle 14.1.55674.0—T1/TP1 and T3 EFILE

The Canada Revenue Agency (CRA) and Revenu Québec have certified TaxCycle T1/TP1 and T3 for filing 2024 returns when EFILE systems open on Monday, February 24, 2025.

To install this version immediately, download the full installer from our website or request a free trial. Once we enable the automatic updates for this version, TaxCycle will prompt you to install it according to the priority set in your TaxCycle Options. (To deploy auto-update files from your network, see the Auto-Update Files page.)

Release Highlights

T1 2024 Ready for EFILE

The Canada Revenue Agency (CRA) has certified TaxCycle T1 2024 for electronic filing when the systems reopen on February 24, 2025. As of that date, you can use TaxCycle T1 to access the following electronic services:

Due to the Department of Finance’s recent announcement as well as Revenu Québec’s announcement regarding the deferral of the increased capital gains inclusion rate, several forms are likely to change. We are awaiting instructions from both the CRA and Revenu Québec on the extent of the changes and the required form revisions. You should not attempt to file, by mail on paper or through EFILE, a return that uses any of these forms until they are finalized and CRA has certified TaxCycle for these forms. The affected forms show the Preview watermark and are included in the list below.

At the CRA’s request, we have disabled the ability to print any returns that have capital gains or losses. This functionality will be restored in a later release.

The following federal forms still show the Preview watermark due to ongoing work:

- Schedule 3 Capital Gains or Losses

- T657 Calculation of Capital Gains Deduction

- T691 Alternative Minimum Tax

- T936 Calculation of Cumulative Net Investment Loss (CNIL)

- T1170 Capital Gains on Gifts of Certain Capital Property

- T1206 Tax on Split Income

- T1237 Saskatchewan Farm and Small Business Capital Gains Tax Credit

- T2017 Summary of Reserves on Dispositions of Capital Property

- T2048 Capital Gains Deduction for Qualifying Business Transfers

- T1A Request for Loss Carryback

- Allowable business investment loss (ABIL) worksheet

- T2203 Provincial and Territorial Taxes for Multiple Jurisdictions and provincial 428MJ forms.

- Schedule 8 Québec Pension Plan Contributions

All other T1 forms are final.

TP1 2024 Ready for NetFile

Revenu Québec has certified TaxCycle TP1 2024. You can use TaxCycle TP1 to access the following electronic services:

The following Québec forms still show the Preview watermark due to ongoing work:

- TP1 Schedule G Capital Gains and Losses

- TP-726.7 Capital Gains Deduction on Qualified Property

- TP-726.6 Cumulative Net Investment Loss

- TP-726.20.2 Capital Gains Deduction on Resource Property

- TP-729 Carry-Forward of Net Capital Losses

- TP-776.42 Alternative Minimum Tax

- TP-232.1 Business Investment Loss

- TP-766.34 Income Tax on Split Income

- TP-22 Income Tax Payable by an Individual Who Carries on a Business in Canada, Outside Québec

- TP-25 Income Tax Payable by an Individual Resident in Canada, Outside Québec, Who Carries on a Business in Québec

- TP-726.30 Income Averaging for Forest Producers

- LE-35 Contribution and Deduction Related to the QPP or the CPP

All other TP1 forms are final.

T3 for 2024

TaxCycle T3 is ready for electronic filing of T3 returns for 2024 with the CRA for tax returns that are not submitting capital gains related amounts.

Capital gains related forms show the Preview watermark, as the CRA has yet to finalize these forms. We are awaiting instructions from the CRA on the extent of the changes and the required form revisions. You should not attempt to file, by mail on paper or through EFILE, a return that uses any of these forms until they are finalized and CRA has certified TaxCycle for these forms. The affected forms are included in the list below.

At the CRA’s request, we have disabled the ability to print any returns that have capital gains or losses. This functionality will be restored in a later release.

To provide additional time for taxpayers who need to report capital dispositions, the CRA is providing relief from late-filing penalties and arrears interest for T3 Trust filings until May 1, 2025. This relief applies to both the filing of T3 information returns (slips) and the T3 income tax return. To learn more, read Update on the Canada Revenue Agency’s administration of the proposed capital gains taxation changes.

The following forms still show the Preview watermark due to ongoing work:

- T3ABIL Allowable Business Investment Loss worksheet

- TPABIL Allowable Business Investment Loss worksheet

- S1 Dispositions of Capital Property

- S1M Capital property disposition manager

- S9 Income Allocations and Designations to Beneficiaries

- S9WS S9 Allocation Worksheet

- S10 Part XII.2 Tax and Part XIII Non-Resident Withholding Tax

- S12 Minimum Tax

- T1055 Summary of Deemed Dispositions

- T184 Capital Gains Refund to a Mutual Fund Trust

- T3RET and Provincial tax and credits forms: T3AB and similar forms will not print and cannot be filed if capital gains related amounts are entered on the return.

All other types of T3 returns or specialty type returns, such as the T3M and T3S, can be filed as usual.

New Forms

We have added the following new forms to TaxCycle T3:

- T1098 Clean Technology Investment Tax Credit

- S130 Excessive Interest and Financing Expenses Limitation

TP-646 for 2024

We are currently awaiting information from Revenu Québec on how to proceed with filing TP-646 returns. As of this release, TP-646 and related forms show the Preview watermark and are included in the list below:

- TP-646 Trust Income Tax Return including schedules A to F

- TP-776.42 Alternative Minimum Tax

- TP-772 Foreign Tax Credit

- TP-653 Deemed Sale Applicable to Certain Trusts

- TP-21.4.39 Cryptoasset Return

- RL-16 Trust Income

T3 Slips Filing Updates

New Boxes on the S9WS and T3BEN

We have added new boxes 52 through 59 related to capital gains changes to the Schedule 9 worksheet (S9WS) and the T3BEN.

Because the CRA is still reviewing and finalizing the Schedule 9, any reported slips amounts in these new boxes may change, and calculations may be altered depending on the CRA’s final changes. This could impact the amounts reported on the T3BEN and Allocation worksheet.

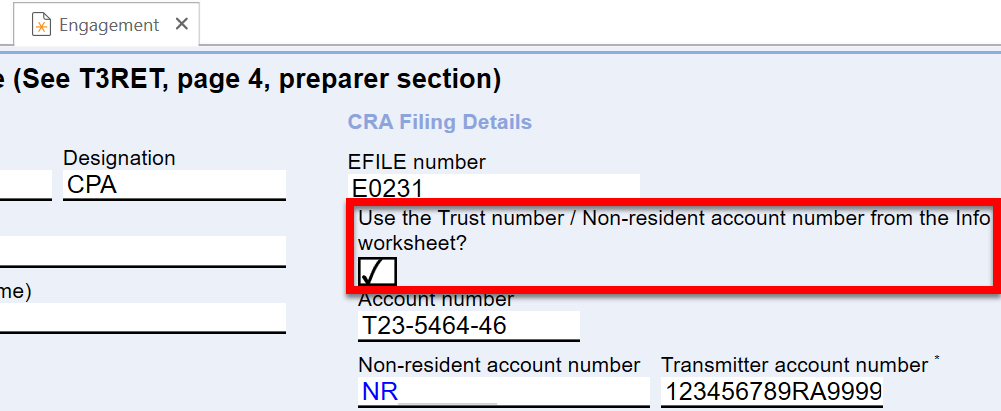

Trust Number as Transmitter Account Number

The CRA now allows (and may require) trusts to use their Trust number as the Transmitter Account Number. The CRA may require trusts to file with their Trust number and an associated Web Access Code (WAC) rather than the Business number/WAC combination that was previously allowed.

You can enter the Trust number directly on the T3 Engagement worksheet, or you can check the box to Use the Trust number from the Info worksheet if your previous 15 character BN/WAC combination does not work.

If both a Trust number and a standard account number are entered, the Trust number will be transmitted to the CRA as the Transmitter account number.

Relief Deadline for T3 Slips

To provide additional time for taxpayers who need to report capital dispositions, the CRA is providing relief from late-filing penalties and arrears interest for T3 information returns (slips) until May 1, 2025. This relief applies to both the filing of T3 information returns (slips) and the T3 income tax return. To learn more, read the CRA’s Update on the filing of information returns.

T3 Schedule 15 and Beneficial Owner Carryforward

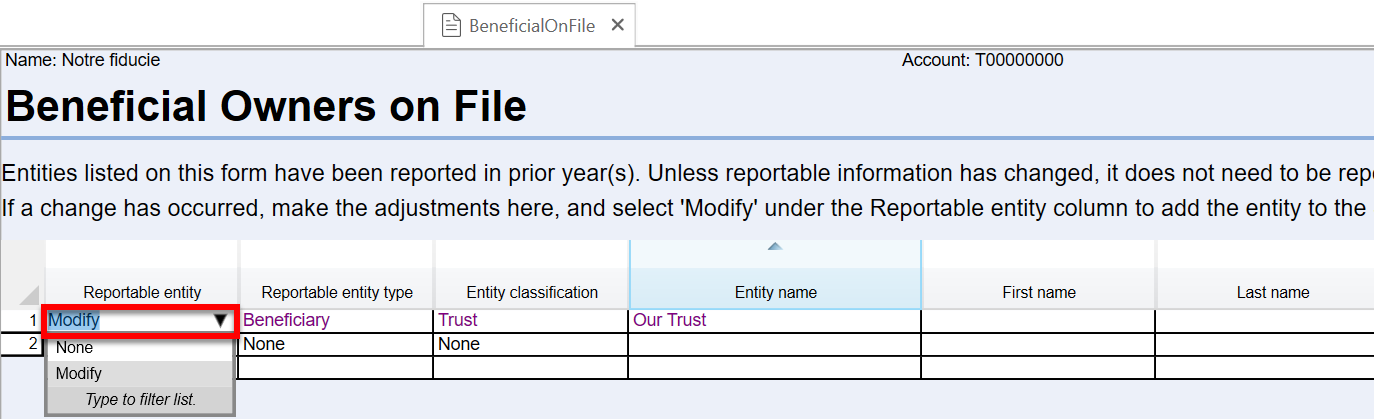

Beneficial ownership information reported on the T3 Schedule 15 in the prior year will carry forward to the Beneficial Owners on File (BeneficialOnFile) worksheet rather than the S15, as parts B and C of the S15 only need to be filled out if you are adding or modifying previously reported beneficial owners (part A of the form continues to require completion each year of filing).

To modify existing beneficial owners on file, open the BeneficialOnFile worksheet and select Modify from the Reportable entity column. The updated beneficial ownership information will flow to the S15.

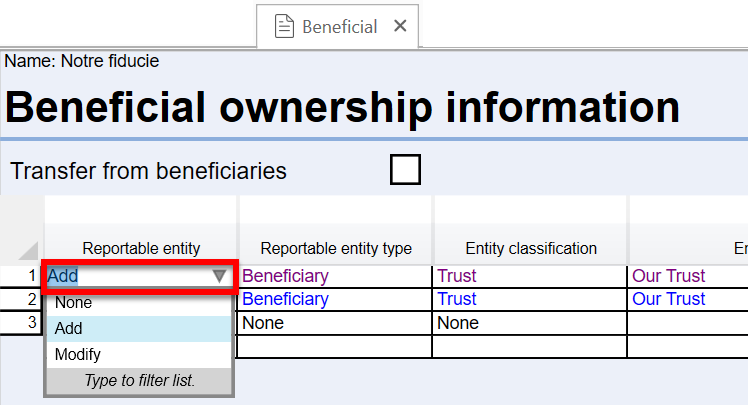

You can add beneficial owners directly on the S15, or by selecting Add from the Reportable entity column on the Beneficial worksheet.

Bare Trust Filing Relief

As per the CRA’s announcement from October 29, 2024, bare trusts are not required to file a T3 return and Schedule 15 for the 2023 and 2024 tax years, unless the CRA makes a direct request for these filings.

The new trust reporting requirements still apply to other affected trusts with taxation years ending after December 30, 2023. These affected trusts are required to file a T3 return, including Schedule 15, unless specific conditions are met.

To learn more, read the CRA’s pages Trust reporting for the 2024 tax year and New reporting requirements for trusts and bare trusts: T3 returns filed for tax years ending after December 30, 2023, respectively.

Resolved Issues

- Customer Reported T1—Fixed a typo in the AuthEmail and AuthRepBusEmail templates for years 2019 through 2024. This affects the English templates only.

- T5013—Known Issue: Attempting to File T5013FIN, Slips and Summaries Results in Error. Please wait to file returns with capital gains or returns which require the new schedules (S75, S78 or S130).

- Customer Reported T5013—Fixed a duplicate calculation in the ACB on carryforward for limited losses applied in the previous year at box 109.

- Customer Reported TaxCycle Forms—Resolved a SERs transmission error related to line 002 for individual taxpayers.

Status of File Carryforwards from 2023 to 2024

As of this release, the following 2023 to 2024 carryforwards are up to date. However, we strongly recommend you only perform batch carryforward on tax modules that are ready for filing in the list, below. We anticipate the rest of the modules will be finalized later in February.

Ready for batch carryforward:

- T1/TP1—TaxCycle, ProFile®, Taxprep®, Cantax®, DT Max®

- T2/CO-17—Carryforwards from TaxCycle, ProFile®, Taxprep®, Cantax®, DT Max®, creating files with year ends up until May 31, 2025.

- T3/TP-646, RL-16—TaxCycle, ProFile®, Taxprep®

- T4, T4A, RL-1/RL-2—TaxCycle, ProFile®, Taxprep®, Cantax®

- T4PS—TaxCycle, ProFile®, Taxprep®, Cantax®

- T4A-RCA—TaxCycle, ProFile®

- T5, RL-3—TaxCycle, ProFile®, Taxprep®, Cantax®

- T2202—ProFile®, Taxprep®

- T5018—TaxCycle, ProFile®, Taxprep®, Cantax®

- T3010/TP-985.22—TaxCycle, ProFile®, Taxprep®, Cantax®

- NR4—TaxCycle, ProFile®, Taxprep®, Cantax®

- Forms—TaxCycle, ProFile®, Taxprep®, Cantax®

- RL—TaxCycle, ProFile®, Taxprep®, Cantax®

Wait for batch carryforward:

- T3/TP-646, RL-16—Cantax®, DT Max®

- T5013/TP-600, RL-15—TaxCycle, ProFile®, Taxprep®, Cantax®

Status of 2024 Federal Returns and Slips

- T1—You may begin data entry. EFILE opens on February 24, 2025.

- T2—Certified to file tax year ends up to May 31, 2025.

- T3RET—You may begin data entry. EFILE opens on February 24, 2025.

- T3 slips—Ready for filing.

- NR4 (in T3 module)—Ready for filing.

- T4—Ready for filing.

- T4A—Ready for filing.

- T4PS—Ready for filing.

- T4A-RCA—Ready for filing.

- T5—Ready for filing.

- T5013-FIN—In progress. Wait to file 2024 returns.

- T5013 slip summary—In progress. Wait to file 2024 returns.

- T5018—Ready for filing.

- NR4 slips (standalone NR4 module)—Ready for filing.

- T4A-NR slips (in NR4 module)—Ready for filing.

- T3010—Ready for filing.

Status of 2024 Québec Returns and Relevés

- TP1—You may begin data entry. NetFile opens on February 24, 2025.

- TP-646—In progress. Wait to file 2024 returns.

- RL-16—In progress. Wait to file 2024 returns.

- TP-600—In progress. Wait to file 2024 returns.

- RL-15—In progress. Wait to file 2024 returns.

- RL-1—Ready for filing.

- RL-2—Ready for filing.

- RL-3—Ready for filing.

- RL-24—Ready for filing.

- RL-25—Ready for filing.

- RL-31—Ready for filing.

- TP-985.22—Ready for filing.