TaxCycle 14.0.55100.0—Major T2/AT1 Update, Capital Gains Inclusion Rate Increase (Retracted)

This release extends the tax year ends for T2 and AT1 returns up to May 31, 2025. It also adds the increased capital gains inclusion rate to the T2 module.

To conform with the CRA's expectations for the draft T2 Schedule 6, we have retracted the full installer for TaxCycle version 14.0.55100.0. Please download a more recent TaxCycle release.

To install this version immediately, download the full installer from our website or request a free trial. Once we enable the automatic update for this version, TaxCycle will prompt you to install it according to the priority set in your TaxCycle Options. (To deploy auto-update files from your network, see the Auto-Update Files page.)

Release Highlights

Revisions

We originally released version 14.0.55054.0 on December 3, 2024, with the changes below, followed by version 14.0.55072.0 on December 5, 2024, as an auto-update. On December 10, 2024, we released version 14.0.55100.0 to resolve the following issues:

T2 and AT1 Extension of Fiscal Year End

This certified release of TaxCycle T2 and AT1 extends the corporate tax year ends up to May 31, 2025.

New T2 Forms

Schedule 75, Clean Technology Investment Credit

- Use this form to calculate your Clean Technology (CT) Investment Tax Credit (ITC).

- The clean technology ITC calculated on line 165 flows to line 155 on the S31.

- The clean technology ITC recapture calculated on line 245 flows to line 25D on Schedule 31 (Part 25).

- The labour requirements addition to tax is calculated on line 430 in Part 4 and flows to line 580 of the T2 return.

Updated T2 Forms

T2 Jacket

- Added a new check box 278 on page 3 for new Schedule 130 (Interest and Financing Expenses Deductibility Limitation). Please note that the CRA has deferred the implementation of the new schedule 130 until the 2025 spring release.

- Added a new line 580 on page 8. This line is calculated from line 440 on the new Schedule 75.

Schedule 1

- Added new line 250, Hybrid mismatch amount under subsection 18.4(4) or 12.7(3).

- Added new line 350, Adjustment for hybrid mismatch amount under paragraph 20(1)(yy).

Schedule 5

- Added new line 329 for the new Manitoba rental housing construction incentive tax credit.

Schedule 6

Schedule 31

- Added line 140 (Clean hydrogen ITC) and line 170 (Clean technology manufacturing ITC) in Part 24.

- The existing line 155 is now calculated from Schedule 75; if you open a T2 file in the new release with an amount on this line, TaxCycle will keep the previous amount as an override.

- Lines 25C, 25D and 25E in Part 25 are new. Line 25C calculates from line 245 in the new Schedule 75.

Schedule 58

- TaxCycle now assigns a transmittable column number of 122 to the previously added column 10 (Qualifying labour expenditure).

Schedule 411 (SK)

- As per the CRA’s request, the calculation of line 1B (“line 400 of the T2 return”) now includes a portion of the amount from line 625 in Schedule 7 to adjust for the difference between the federal and Saskatchewan small business deduction limit ($500,000 vs. $600,000).

- For example, if the amount in line 625 is $100,000, the incremental portion of $20,000 ($100,000 x ($600,000 / $500,000)) is added to the calculation of line 1B in Part 1 of Schedule 411.

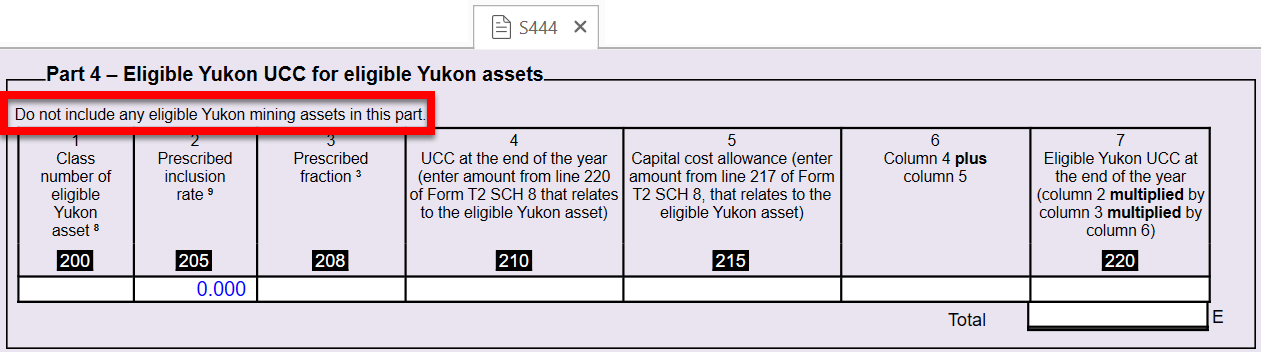

Schedule 444 (YT)

- When a corporation’s tax year starts on or after 2024, TaxCycle shows the new version of the form. Otherwise, TaxCycle will show the previous version of the form.

- Updated to take into account Yukon’s Bill 34, where a technical deficiency was fixed with respect to the calculation of Part 4. If a corporation’s tax year starts on or after 2024, the Part 4 table must not include any eligible Yukon mining assets.

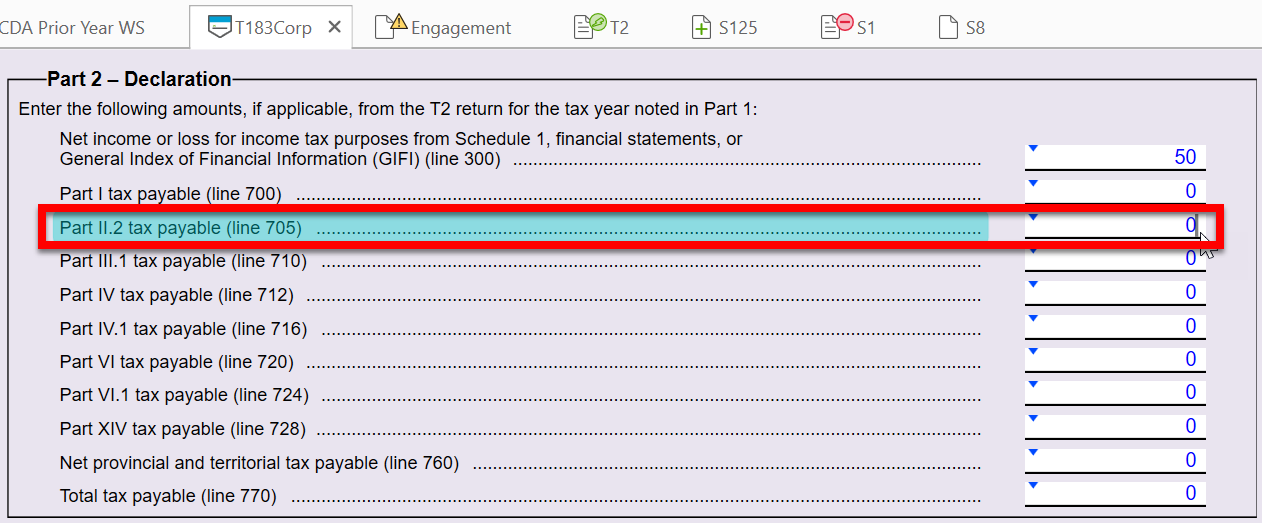

T183Corp

- Part 2 now incorporates a new field to account for Part II.2 tax payable (line 705 in the T2 jacket).

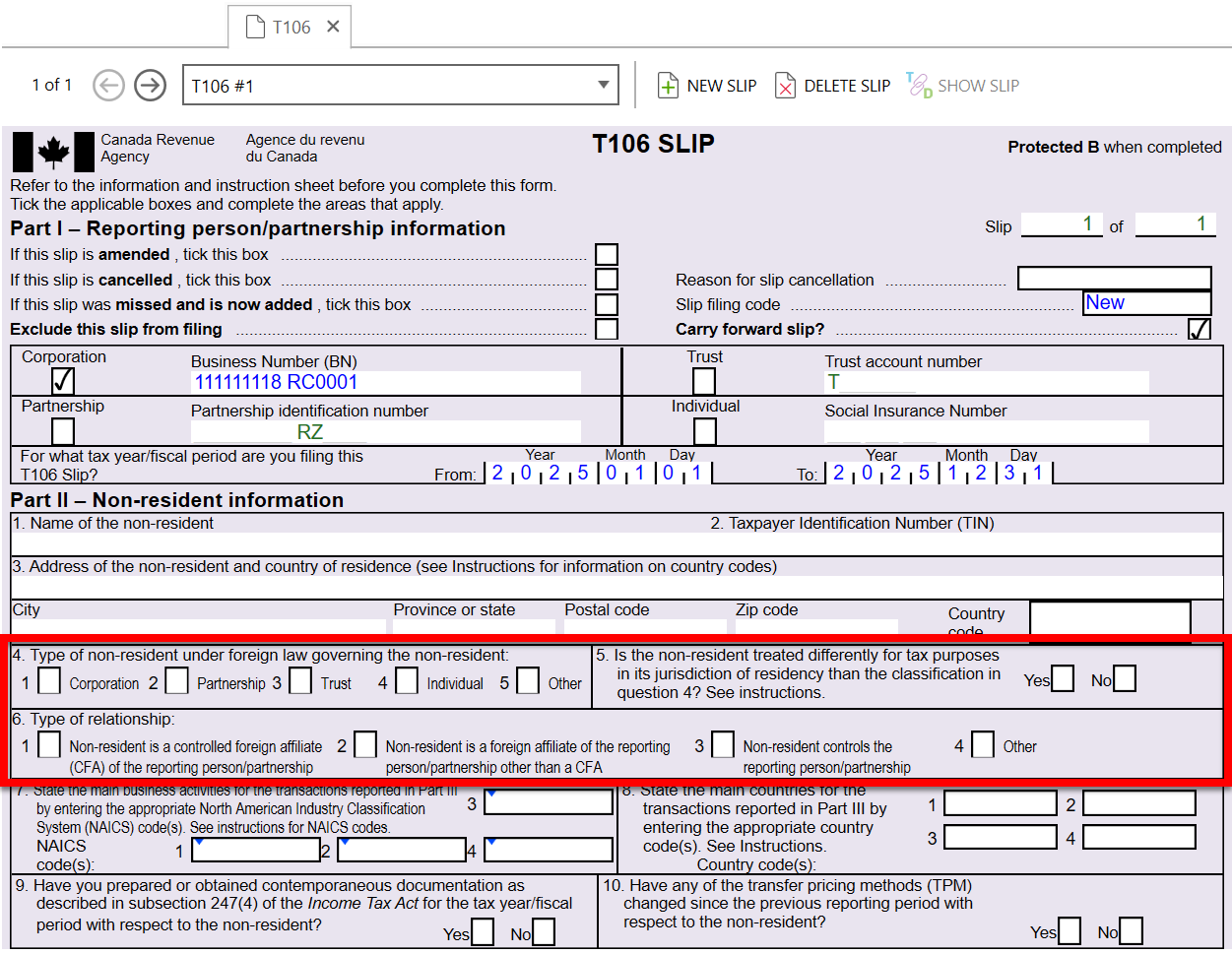

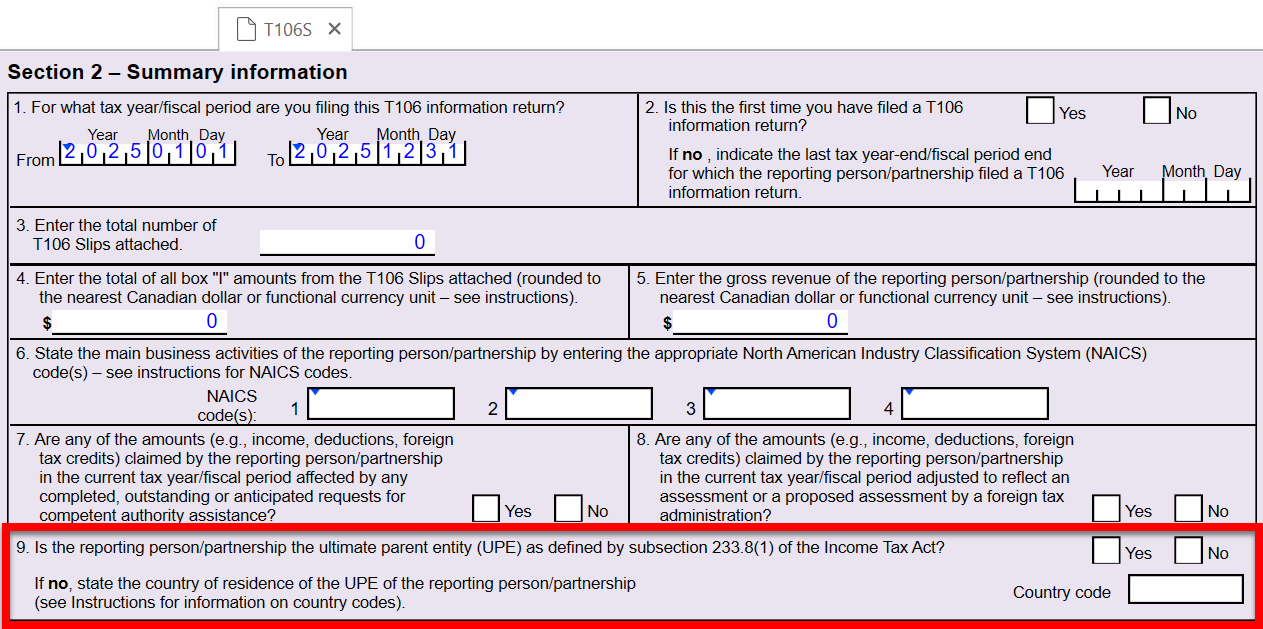

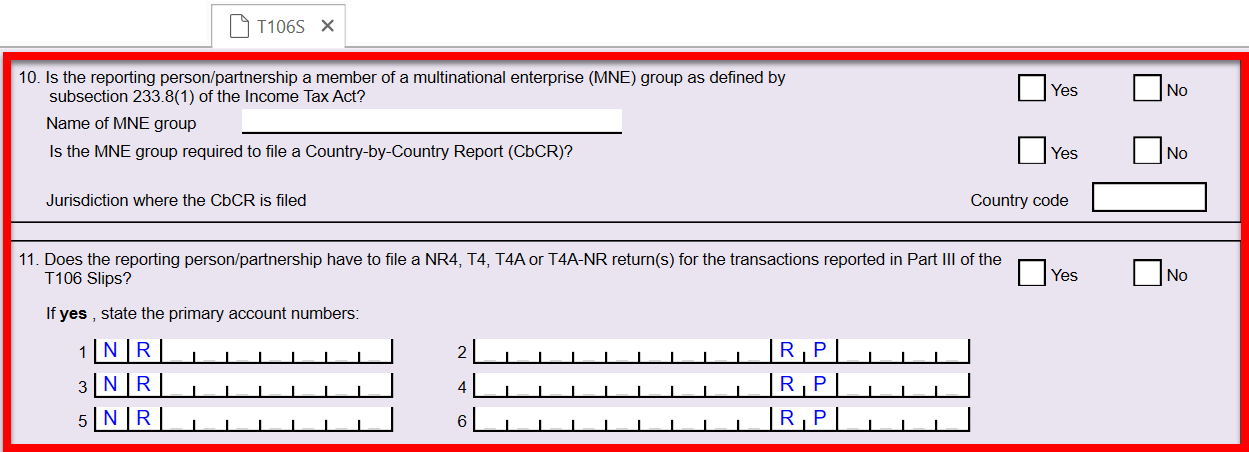

T106

- TaxCycle displays a new version of this form if the tax year starts in 2025 or later.

- The 2025 version of the form contains the following new sections and fields on the T106 and T106S:

Minor Updates

The following forms received minor updates:

- Schedule 54

- Schedule 56

- Schedule 349 (NS)

- Schedule 350 (NS)

- Schedule 421 (BC)

- Schedule 422 (T1196) (BC)

- Schedule 423 (T1197) (BC)

- Schedule 428 (BC)

- Schedule 430 (BC)

Alberta AT1 Updates

Mandatory AT1 Net File

For taxation years beginning January 1, 2025, and later, electronic filing of the AT1 is required for all corporations except for insurance corporations, non-resident corporations, corporations reporting in functional currency, and corporations that are exempt from taxation under section 35 of the Alberta Corporate Tax Act (ACTA).

The Alberta Corporate Tax Act (ACTA) requires prescribed corporations to file the AT1 return electronically, which must be done using the Net File service. The definition of “prescribed corporation” in the Alberta Corporate Tax Regulation was recently amended to remove the exception for corporations whose gross revenue exceeds $1 million.

Accordingly, for AT1s in respect of taxation years that begin after December 31, 2024, all corporations will be required to file electronically using the Net File service except:

- insurance corporations

- non-resident corporations

- corporations reporting in functional currency

- corporations that are exempt from taxation under section 35 of the ACTA.

AT1 Jacket

- Added two new check boxes to line 030 on page 1: Insurance corporation and Non-resident corporation. These check boxes calculate based on the special corporation status field entered on the T2 Info worksheet.

AT1 Schedule 29 (AS29), AS29Steps, and the AS29 section in CGI Worksheet

- Removed lines 120, 122 and 124 from AT1 Schedule 29.

- Added new columns 235, 245, 267 and 268 to the allocation limit table on the last page of the AT1 Schedule 29. Also added these same columns to the AS29 allocation table on the CGI worksheet.

- Added new total fields (lines 310 and 320) to the allocation limit table on Schedule 29.

- TaxCycle now calculates the reporting corporation’s allocated limit on the new line 325 and carries it over to line 125.

- Revised the AS29Steps based on the information included in the Alberta Corporate Tax information circular IEG-1.

Other Updates

- Customer Request T1 2023—As requested by a customer during the latest Ask Us Anything webinar, we have added a new review message that appears when the downloaded AFR data indicates the CRA has uncashed cheques on file for the client.

- T1 2024—TaxCycle no longer shows a paragraph about not being required to file a bare trust T3 return in the client letter (CLetter) and joint client letter (JLetter) when you answer “No” to the question about bare trust filing on the Engagement worksheet.

- T1 2024—TaxCycle now shows the name of the signer in the signature field and in a banner on the T1032 when there are multiple signers.

- T3—Updated the e-signature functionality for the T183Trust to align with the T183 in T1, ensuring consistent behaviour when sent for e-signature and signed by the client.

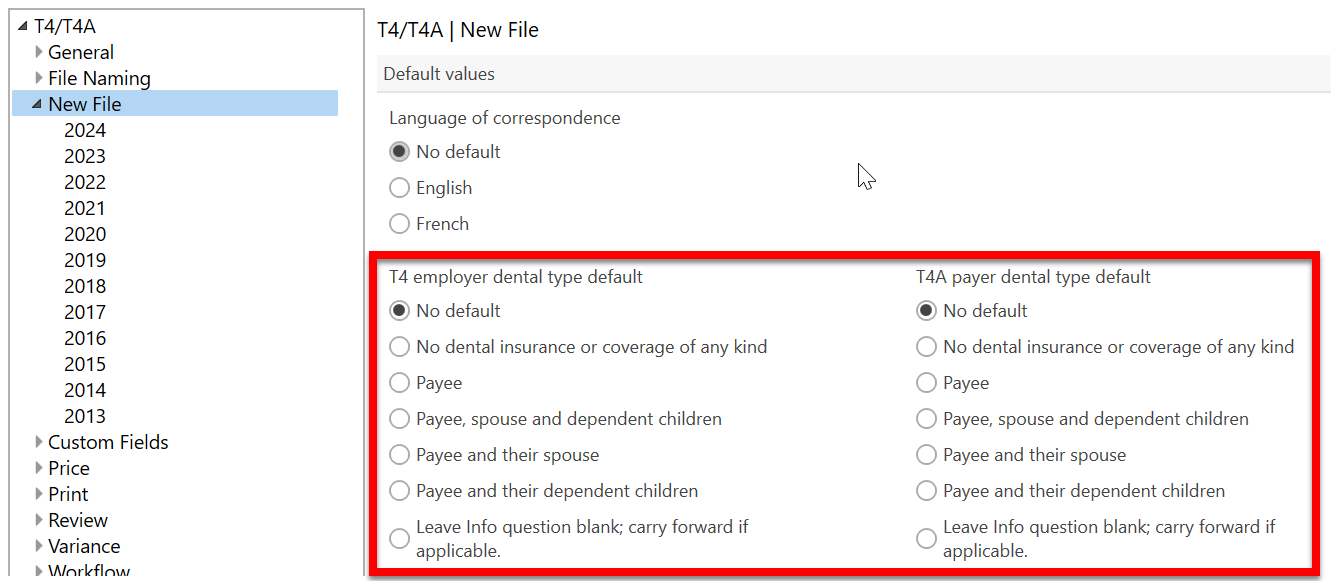

- T4 2024—Added new Options to the T4/T4A module to determine how TaxCycle will handle the employer-offered or payer-offered dental benefits. T4 box 45 and T4A box 15 were newly added in 2023 and the new options will determine how TaxCycle handles the question when creating or carrying forward a return. The default option is “No default.”

- T5013—T1134 and T1135 are now certified for year ends up to and including May 31, 2025.

Resolved Issues

- Customer Reported T2—Fixed an issue where TaxCycle displayed the wrong tax year on the T2183 when filing the CDA Next Year worksheet (T2054) using SERs.

- Customer Reported T2 and Forms module—Updated the “payment required” review message that appears on SERs forms in TaxCycle T2 and TaxCycle Forms to only show when there is a payment amount owing on the applicable form.

- Customer Request T5013—Resolved an issue where new T1134 slips were not defaulting to “Missed and now added” when amending an already filed T1134 return by adding a new slip.

- Customer Reported Client Manager—Fixed an issue where the Client Manager was not correctly sorting the transmission confirmation number and date columns in search results.

- Customer Reported Client Manager—Resolved an issue where the Client Manager was not indexing 2023 T1 returns from Taxprep®.