Additions in CCA classes 44, 46 and 50 acquired after April 15, 2024, are resulting in 100% of CCA being claimed.

In the April 2024 federal budget, the Department of Finance announced an accelerated Capital Cost Allowance (CCA) measure for “productivity-enhancing assets.” The proposed measure states that the CCA for classes 44, 46 and 50 will be fully written off for additions made after April 15, 2024, and before January 1, 2027, by grossing the Undepreciated Capital Cost (UCC) of the additions using multipliers of 3, 7/3 and 9/11, respectively.

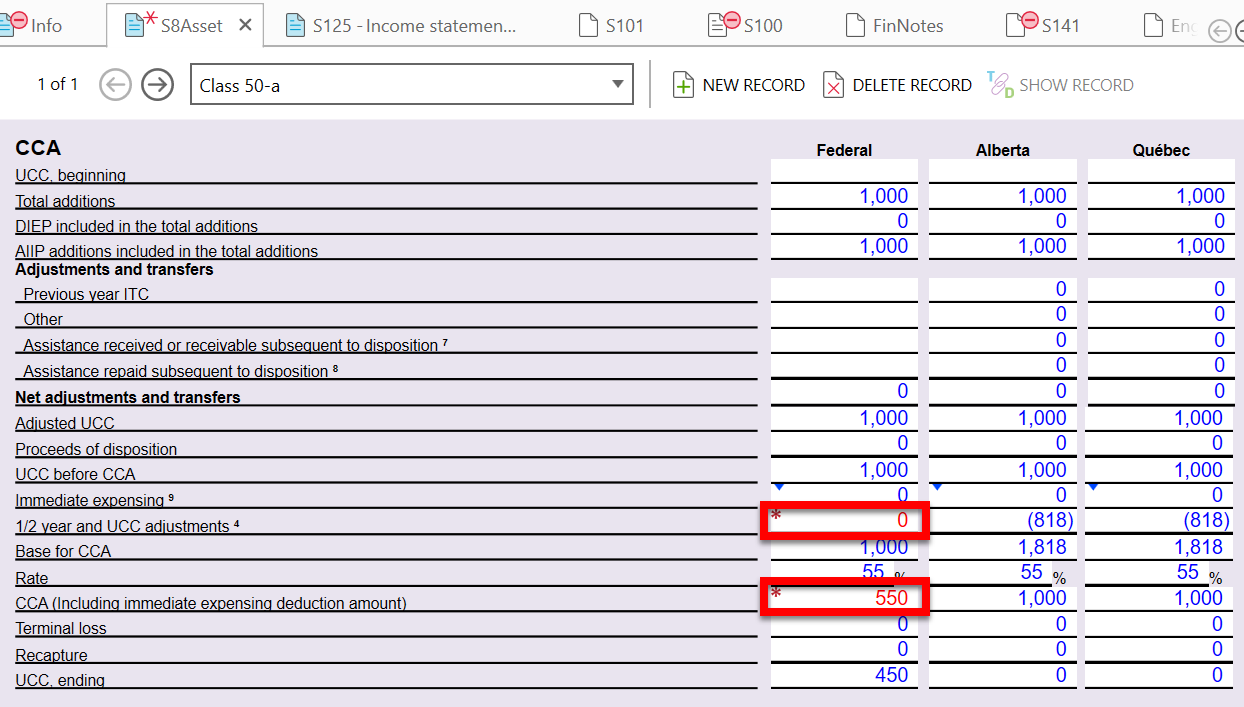

We implemented this measure in a previous TaxCycle release. However, since the proposed measure has not yet been enacted, CCA calculations should not fully claim CCA for additions made after April 15, 2024.

For example, for an addition of $1,000 to class 50 on May 1, 2024, the CCA should be calculated as $550 ($1,000 × 55% = $550). The class 50 addition is eligible to be classified as Accelerated Investment Incentive Property (AIIP). As part of Phase II of the AIIP rule, originally announced in 2018, the half-year rule must continue to be suspended, and the CCA rate is applied to the addition without grossing up the UCC. However, in addition to applying Phase II of the AIIP rule, TaxCycle is also applying the proposed “productivity-enhancing assets” measure, which should not be considered in the CCA calculations.

Manually override the UCC “gross up” and CCA on the S8Asset.

We resolved this issue in the latest TaxCycle update.